The expansion of Renewables and its 1,000B€ argument for connectivity

As the world transitions gradually to renewables, and the energy storage technologies do not keep up, the flexibility solutions are now scaling thanks to the availability of the required technology bricks and boosted by a staggering market potential.

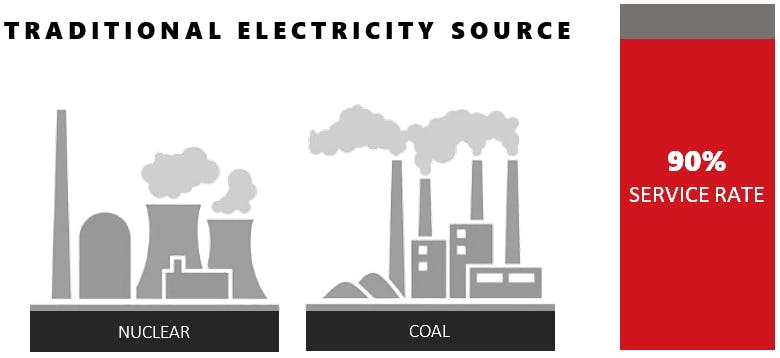

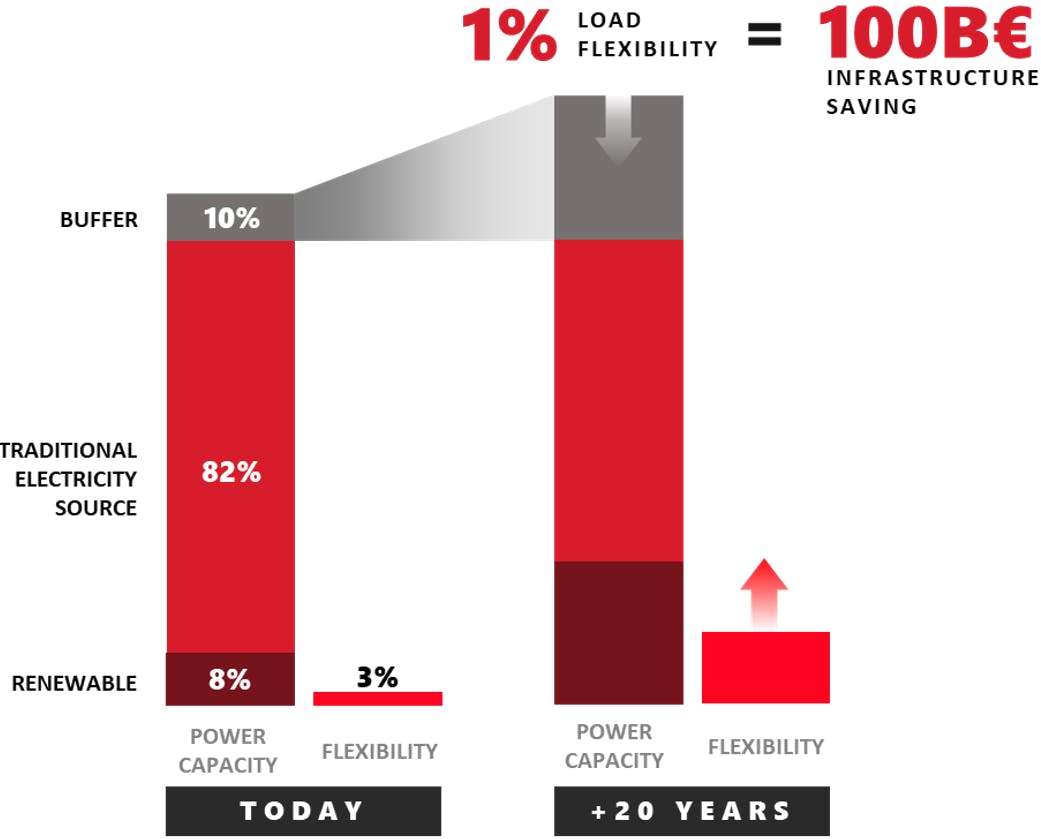

The drawback of renewable energy sources, such as wind and solar, is well known: their supply is intermittent with an average service rate of 30%. It means that when you build a renewable energy plant with a maximum power capacity of 10, in average you get 3. This is radically different from the legacy energy sources which have an average service rate of 90%.

If the balance mechanisms between demand and supply were to stay the same, renewables would require a significant increase in grid buffer capacity. A great number of gas, coal, nuclear plants with high service rate would need to be built or refurbished to jump in at peak imbalance times.

Power capacity costs a lot. Flexibility on the demand side is the mechanism which allows to minimize the grid buffer size. At the world level, each additional percentage point of flexibility saves 100B€ in electrical infrastructure construction. Therefore, states and TSOs are well decided to minimize the additional buffer capacity requirements. To this end, new demand response programs are springing up like mushrooms.

The demand response concept is like the practice of flight overbooking: a consumer gets a compensation for a change of plan. Everybody wins: the provider maximizes its usage rate, the average consumer is offered a better price thanks to an overall lower service cost, and the consumer who accepts the change of plan gets a good deal.

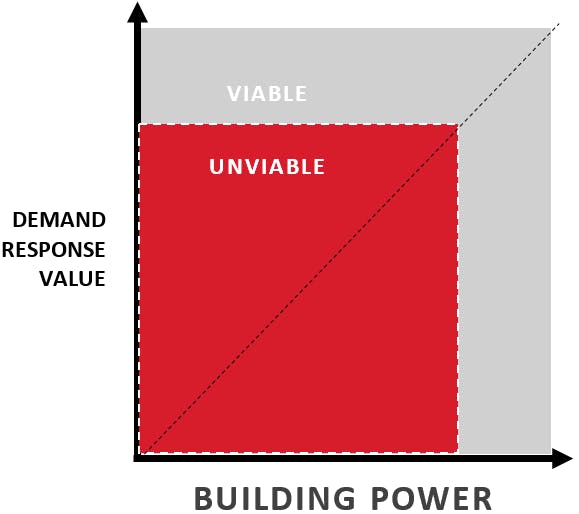

And it all boils down to:

- The demand response value creation from the site

- How much inconvenience goes with the change of plan

- How much it costs to control the power of the site

Every site is a potential flexibility source for energy aggregators. As an example, a convenient store might be a small load at the grid level, but the combination of all of them is something else. The viability of going down to even smaller sites, like homes, is questionable. The expansion of technologies such as IFTTT will certainly help on the control cost but the value creation might not be that big due to low occupancy at peak times and the inconvenience of change of plan which is high in household applications.

In the case of building HVAC systems which have by nature high inertia, the inconvenience of change of plan can virtually be zero through smart software anticipation which takes in consideration weather forecast, building dynamic, usage behavior, and so on. The HVAC is the best and biggest flexible load which can be found.

What then remains in the demand response equation is the cost to control the power of the site. There are 2 potential situations in C/I/I buildings (commercial, industrial and institutional):

- There is a Building Management System: it needs to be made accessible from the web

- There is no BMS: a web connected BMS must be built

When looking at the market size, one could expect that the building demand response solutions would come from the industry giants such as Siemens, Schneider or Honeywell. But instead, the demand response applications are shipped by agile organizations all over the world, most of them having software engineering at their core.

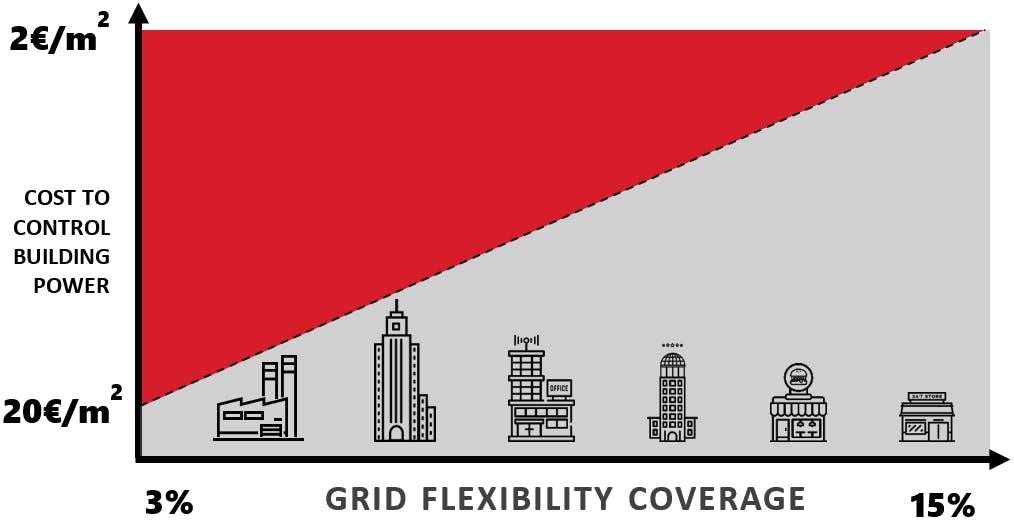

These organizations are confronted with the legacy BMS infrastructure which is not exactly the web app best friend. The cost and complexity of BMS web connectivity is the largest limiting factor for demand response scalability.

The transition to renewable energy sources requires the deployment at scale of demand response apps into millions of buildings. Extending the coverage of flexible loads from today’s 3% to 15% in 20 years has the potential of saving over 1,000B€ in grid infrastructure construction.

In the end there is no big surprise. Nothing new in the increasing necessity of smart grids to better balance demand and supply. One technical and economical consideration though is that increasing the smartness of the consumer loads requires the BMS infrastructure to be re-invented. A simple, secure, scalable and affordable BMS connectivity will support the energy transition by lowering the cost of renewable power production. We are working on it:

Wattsense Products

From an era of gateways, PLCs, automation engineers, and VPNs to a plug & play connectivity service.

When the energy storage technology matures, the combination of HVAC flexibility and batteries will complement one another to further reduce the grid buffer size and push toward a world with full renewable energy supply.

Want to learn more about the Wattsense connectivity solution?

Discover our solutionContinue reading